Chile’s wind sector has moved from rapid expansion to a stage where system integration is becoming the central challenge. According to Felipe Gallardo, Research Director at the Chilean Association of Renewable Energy and Storage (ACERA), the country’s progress in building wind capacity is now being matched by the need to adapt infrastructure, regulation and market design to support a highly renewable electricity system.

Chile’s wind sector has moved from rapid expansion to a stage where system integration is becoming the central challenge. According to Felipe Gallardo, Research Director at the Chilean Association of Renewable Energy and Storage (ACERA), the country’s progress in building wind capacity is now being matched by the need to adapt infrastructure, regulation and market design to support a highly renewable electricity system.

By Felipe Gallardo, Research Director, Chilean Association of Renewable Energy and Storage

A Power System in Rapid Transition

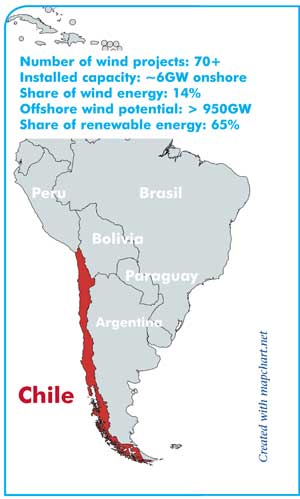

Over the past decade, Chile’s electricity sector has undergone a structural shift away from its historical reliance on hydropower and thermal generation towards renewable energy. By 2025, renewables accounted for approximately 65% of electricity generation, reflecting both policy direction and sustained private investment.

Wind energy has been a key contributor to this change. The country now has around 6GW of installed onshore wind capacity, distributed across more than 70 projects. Over the last five years, the sector has expanded at an average annual rate of around 21%, making wind one of the fastest-growing technologies in Chile’s generation mix. It currently supplies about 14% of national electricity demand.

This growth has been underpinned by strong wind resources, a competitive electricity market, and a regulatory framework that has enabled deployment without direct subsidy schemes. International and domestic investors have both played a significant role in scaling the sector.

From Early Deployment to a Mature Industry

While Chile’s early wind projects date back to the early 2000s, large-scale commercial development is a relatively recent phenomenon. The acceleration over the past decade has been supported by declining technology costs, improved grid regulation, and national decarbonisation targets.

The sector has now evolved into a mature industry with a broad ecosystem of participants. These include global turbine manufacturers, independent developers, utilities, financial institutions, and a growing base of specialist service providers. This industrial structure has supported the integration of Chilean wind power into global renewable energy value chains and strengthened project delivery capabilities within the country.

Continued Growth Potential

Despite strong growth to date, Chile’s wind market still holds significant expansion potential. Several analyses indicate that the country may require around 18GW of additional wind capacity over the coming decade to align with decarbonisation pathways and rising electricity demand.

Onshore wind is expected to remain the dominant technology in the short to medium term. However, hybrid projects combining wind generation with energy storage are increasingly being developed as system flexibility becomes more important.

Offshore wind represents a longer-term opportunity. With a coastline exceeding 4,000 kilometres, Chile has estimated offshore wind resources of more than 950GW. Development is expected to rely largely on floating technology because of deep-water conditions, although this remains at an earlier stage of global maturity.

Electrification as a Demand Driver

Beyond generation expansion, a key structural opportunity lies in electricity demand growth. At present, only around 23% of Chile’s final energy consumption is electricity, indicating substantial scope for electrification.

Industrial sectors are expected to be central to this shift. Mining, data centres, industrial heat applications, and green hydrogen production are all anticipated to drive future electricity demand. This evolving demand profile is likely to reshape investment priorities and increase the importance of system flexibility.

Integration Challenges Emerging

As wind and solar capacity continues to expand, Chile’s energy transition is increasingly constrained not by resource availability, but by system integration.

Transmission infrastructure has become a critical bottleneck. Renewable generation is often concentrated in resource-rich regions far from major demand centres, limiting efficient power transport across the system. This has contributed to growing levels of renewable curtailment, particularly during periods of high solar output in daytime hours.

System flexibility is another pressing issue. In the absence of sufficient storage capacity and demand-side adaptation, oversupply events can lead to very low or even zero wholesale electricity prices. This creates challenges for revenue stability and investment signals across the sector.

Additional constraints include land availability, territorial planning complexity, environmental permitting processes, and logistical limitations in transporting large turbine components. These factors are becoming increasingly relevant as project scale increases.

Recent experience suggests that continued renewable expansion will require parallel investment in transmission networks, storage infrastructure, and regulatory mechanisms that support operational flexibility and system reliability.

Investment Conditions Remain Robust but Evolving

Chile continues to be regarded as an attractive renewable energy investment destination. Its combination of high-quality natural resources, stable institutional conditions, and established project development track record underpins strong market fundamentals.

However, investment dynamics are becoming more complex. Future competitiveness will depend less on resource quality alone and more on the ability to manage congestion, price volatility, and regulatory adaptation.

At the same time, new investment opportunities are emerging beyond traditional generation assets. Energy storage, green hydrogen development, and electrification technologies are increasingly seen as key growth areas, offering new ways to monetise renewable energy production.

Towards a Highly Renewable System

Chile has set long-term policy objectives, including coal phase-out by 2040 and carbon neutrality by 2050. Within this framework, wind energy is expected to play a stabilising role by complementing solar generation, particularly during evening and night-time periods.

However, achieving full decarbonisation will require more than continued capacity expansion. It will depend on the development of a coordinated energy system in which generation, transmission, storage and demand evolve together.

According to analysis from ACERA, the next phase of Chile’s energy transition will be defined by system design rather than build-out alone. If these structural challenges are addressed, Chile could reinforce its position as a leading renewable energy market in Latin America and provide a reference point for other countries facing similar integration pressures.

Windtech Markets is a collaboration between Windtech International and the World Wind Energy Association and is based on the WWEA Podcast.

Map created with mapchart.net

")